IR35 in Focus with Mark Thomas Part 1

A lot has changed since our first IR35 article. In this two-part post, Mark Thomas discusses important IR35 developments.

Find out more about IR35 from our experts.

Neem contact opIt has been roughly 18 months since I wrote the opinion article IR35 is coming to the Private Sector in ERP Today magazine (Vol. 1, Issue 2).

Since sharing the last article, we have had an expert opinion on the digitalisation of tax compliance as well as an expert opinion on modern tax technology.

Of course, these opinion articles were all in a pre-COVID-19 world, with the subsequent articles sharing this last page being pandemic-focused. This trend has been followed in the world more generally, with IR35 being no exception.

Previously, I focused on the forthcoming legislation changes within the private sector called Off-Payroll (IR35) Working Regulations, which were delayed from the original implementation date of the 6th April 2020 and pushed forward by a year to the 6th April 2021 — rightly, as a result of the then increasing threat of COVID-19 and the unprecedented international lockdown.

I will break this article into two parts, as I want to touch on my opinion in two separate areas:

Part 1. How did the first lockdown play into the hands of this legislation?

Part 2. Has the Government failed in areas of the drafting of this legislation?

By the time it was announced by HMRC that the implementation date for the legislation would be pushed back by one year, a large proportion of companies had already invested heavily in their approach. In the main, we saw these organisations continue down their chosen path, typically:

The blanket-banning of PSC contractors was largely (but not exclusively) taken by the Financial Services and Professional Services Industries and large multi-national organisations, leaving smaller organisations with an approach more akin to the spirit of the legislation.

In a post-pandemic world, we believe that organisations operating a blanket ban approach will struggle to attract and retain the highly skilled contractors needed to deliver business-critical IT projects in our world of ERP business applications.

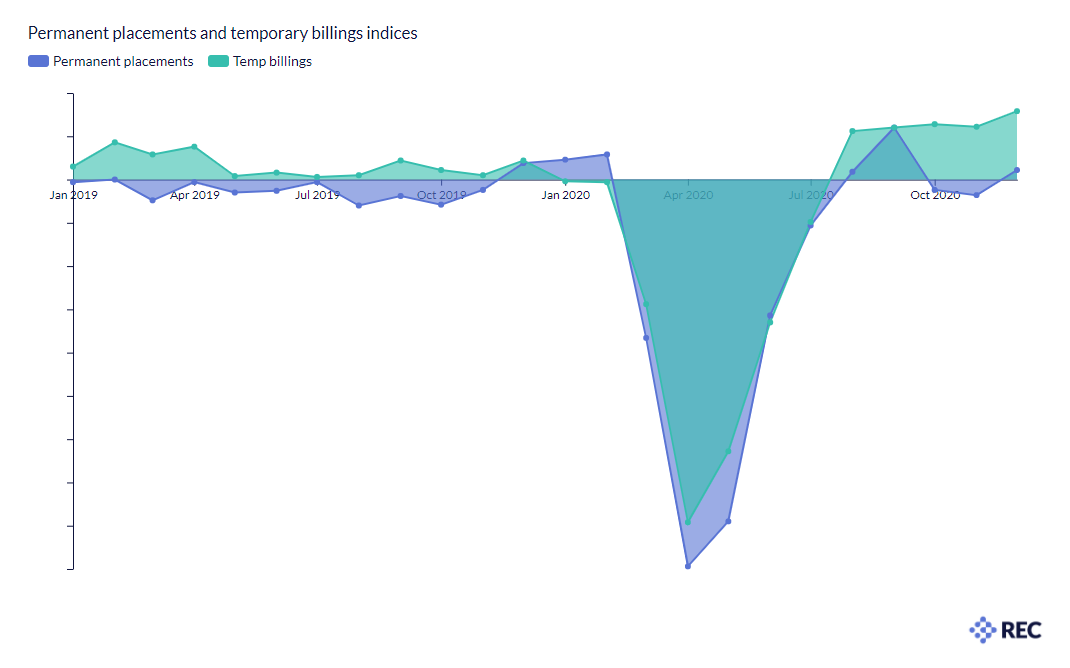

But the fact is that during the period January 2020 – July 2020, a vast number of contractors saw their current projects paused and very few new projects starting, meaning that the market flooded with previously unseen numbers of contractors without assignments.

This trend is documented in the IHS Markit permanent placement and temporary billing indices as illustrated below and available on the Recruitment & Employment Confederations website:

The reality of this scenario is that contractors had little or no choice but to accept ‘inside’ IR35 assignments with far lower net remunerations to maintain an income stream. I believe that this is a false trend that we are already starting to see reverse itself!

Since August 2020, there has been a notable increase in new contract opportunities, which is mirrored in the IHS Markit permanent placement and temporary billing indices.

Since August 2020, there has been a notable increase in new contract opportunities.

The result is that we are now seeing an increased reluctance from contractors to accept ‘inside’ IR35 assignments where there has been no ‘due process’ in terms of the “hiring organisation” employing a documented and sensible ‘Status Determination Statement’ process. In the case of a genuinely determined ‘inside’ IR35 status, we are seeing an increase in the rates charged by the contractor (we touch on why later).

This trend will continue to grow as the IT industry comes to terms with the fact that critical IT projects have to continue. The forced change to contractor working practices has shown that IT projects can continue (and continue successfully) with a majority remote workforce over the past three months!

Organisations which are not operating in the spirit of the legislation and blanket banning ‘outside’ IR35 contractors by not operating a Status Determination process, will alienate themselves from highly skilled contractors. Organisations will then not utilise those niche contractors required to deliver their business-critical IT projects successfully.

Therefore, in summary, we believe that over time the market will settle down with genuinely ‘outside’ IR35 assignments becoming more prevalent as the commercial world re-balances back to the normal market forces and demands.

Mark Thomas FIRP

Corporate Sales Director

The Ellis Recruitment Group

Read the second part of this series: Has the Government failed in areas of the drafting of this legislation?

This article was written by Mark Thomas FIRP, who is a Director of Oracle Contractors and leading their IR35 initiatives. If you would like to discuss this subject further, then Mark can be reached at IR35@oraclecontractors.com.

Our IR35 comparative calculator shows the financial implications of IR35 tax legislation in relation to working inside or outside IR35.

IR35 Comparative Calculator